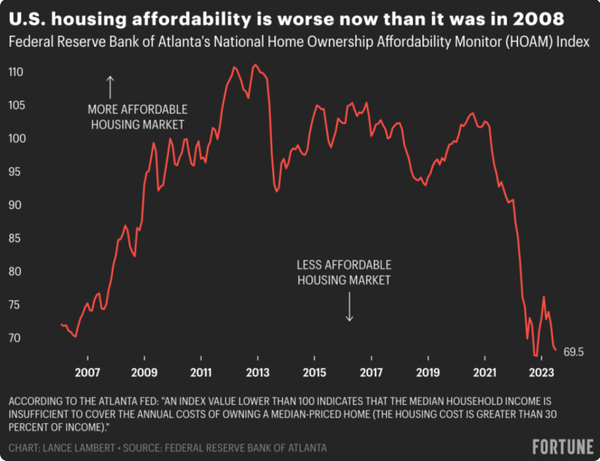

Opinion: As development costs skyrocket, a call to publicly finance Portland's BDS

The City of Portland has announced an increase in building permit fees by 10% in July – greater than current inflation rates - and Multnomah County is considering a similar increase. This continuous march toward ever-rising public costs in new housing construction perpetuates a bloated and broken system with no relief in sight. Before the Portland City Council’s approval of this recent increase, the director of the Bureau of Development Services voiced concern about the unsustainable nature of BDS funding, and in addition to a fee increase asked for an allotment from the city general fund to stabilize the bureau and forestall yet another cycle of firing and hiring based on variable market conditions. The latter request was denied. Consequently, we face a negative ripple effect on both homeowners and home builders, exacerbating the home affordability crisis. As a realtor, retired from structural engineering, I’ve seen people struggle with the effects of a real estate market constrained by increasing costs and a system that creates a disincentive for new home building. I believe we must address the inherent flaws in this self-perpetuating system and consider alternatives, including whether there is a way to publicly finance city or county development services instead. We’ve underbuilt since 2008, both locally and nationally, pushing prices up and making it a challenge for builders to turn a profit. With interest rates at a 10-year high, builders’ holding costs have risen accordingly, along with all the other costs of new construction: land pricing (location-dependent), soft costs (architectural and engineering drawings), labor pricing, material costs, selling fees, and permit fees and SDC charges. Correspondingly, the rising cost of building new homes affects the cost of existing homes, too. Even homeowners with a low interest rate face an unpleasant surprise when they go to purchase their next home and find prices that have escalated thanks to the increasing fees and charges applied in the market overall. Insurance rates & labor markets are also affected by inflated home values driven by the increased cost to build more housing. Using general fund or other non-fee resources to stabilize permitting functions and create greater efficiencies will incent existing builders, lower the cost of entry for entrepreneurs who want to build new housing, and spur new construction even with the current interest rates. Despite the pleas of multiple development groups and business advocates, the increased fees are moving ahead. But let’s keep the conversation going to pause fee increases and explore alternate funding for permitting for the benefit of our housing market and local economy.

Read More

What the Market is doing in April.

Our expectations regarding the market incentives created by low interest rates came into focus in the first 13 weeks of the year, with listings (supply) off sharply from the year prior. We ended the quarter with the gap between this year and last growing wider, a signal that appears to indicate continued low transaction velocity heading into 2Q. This lack of supply appears to have stabilized pricing, and along with seasonal adjustments that look familiar, both median price and percent paid to asking bottomed in January and improved in February and March. Properties below the median now sell, on average, for 100.3% of asking price. Days on market also declined month-over-month for the entirety of the first quarter, now down 18% from the high in January. On the all-important subject of interest rates, inflation continues its steady (but slow) decline, and the last several months give reason to believe we are largely past rate increases. Below we see the annualized rate of inflation, average 30-year mortgage rate, and the real world rate taken by subtracting the yield on the 30-year mortgage from inflation. For nineteen months real world rates remained negative, that is the return on a 30-year mortgage was less than the rate of annualized inflation. As inflation fell and rates rose, real world rates turned positive in December and continue to improve. This is a welcome indication that interest rates are stabilizing and will fall along with inflation as we progress through the year. Bottom line: - The influence of low interest rates on sellers continues to impact supply - Buyer demand remains strong – absorption is in the 95-100% range and DoM is falling - Properties now sell on average for 100% of asking price - Without additional shocks to the system (i.e. bank failures, etc.), interest rates appear to have stabilized and there is a solid basis for expecting them to fall in the coming months - Housing is not going to become more affordable in the near future, as prices are reacting quickly to lack of supply and abating rates Stable pricing and low velocity – we have an interesting year ahead.

Read More

What is Structural & Forensic Engineering- Explained

What is a structural engineer? Some of you may know, some of you may not. Super easy explanation. If the human body was a building, the structural engineer would be the guy designing the bone structure. What is a forensic engineer? It's the individual who figures out what the problem is in building when there's symtoms of greater problems. Kind of like a doctor who figures out why you're not feeling well.

Read More

Recent Posts