September Newsletter- The tale of two markets & Saving your foundation!

It’s the end of September and I think we’re officially in fall with the rain starting. The kids are back in school, and the chanterelles should be popping up this week for any of you that are mushroom enthusiasts! Tip of the month: A gentle reminder to make sure your gutters and downspouts are clear and working properly for the rainy season. If you have a home that the downspouts have been disconnected from the sewer system, make sure the water is draining at least 10’ away from the house. Most homeowners don’t know the consequences of a failed foundation due to an overflowing gutter or a downspout draining next to the home. Over the last month I’ve helped a handful of buyers with identifying failed foundations, and dry rot issues. A good number of these, the home inspectors didn’t catch, and I needed to bring it to their attention & explain what was causing the problem. That “rule” that if a crack in a foundation is less than an 1/8” than it’s not an issue, is not true. Generally, a small crack is a sign of a problem that’s beginning, or several small cracks can be a problem that has been going on for a while. Best practice is talk to an experienced structural engineer to figure out what’s going on and what the fix is or lean on me before listing your home. An engineer may cost money up front, but they’ll also save you significant money on the repair. Without naming names there’s several construction companies out there that overcharge significantly for their services or pad the estimate with items that aren’t required. Why try to figure this out before a home goes to market? A. It can derail a transaction, and you have a sale fail on record which typically results in a home selling for less. B. The repairs tend to be more expensive in the middle of a real estate transaction, and unless your realtor has a background in structural engineering and/or construction, you’re most likely going to be overpaying or paying for things that aren’t needed. I’ve witnessed sellers and their realtor give more away in repairs than what the realtor’s commission was. On the market: The Real Estate market is interesting right now. It’s really the tale of two markets. We’re still seeing multiple offers and bidding wars on certain houses. The homes with multiple offers received are the ones that have been accurately priced and in desirable locations. If a house is still on the market after a week, then the realtor missed accurately pricing it. At which point, the seller should expect to have a price reduction and give concessions to the buyer. So accurately pricing homes is super important, and I think we at Eleete do a great job at this. For the homes that missed the mark, I’ve been able to get sellers to pay for my buyers closing costs, mortgage rate buydowns, plus major repairs. On the rate buy downs: They can either be permanent or temporary. With the current mortgage rates this is a good strategy to help buyers bypass the peak of the mortgage rates and lower their monthly payments till they want to refinance. Some mortgage companies have offers to not charge for their end of the refinance if it’s done within 2 years of the closing. It’s worth asking your lender about what’s possible with what they’re offering. There are some nice homes on the market right now that would’ve been in bidding wars a couple of years ago with inspections being waived. Have a great end of the month and start of the fall season! Feel free to reach out to me anytime, I’m happy to help!

Read More

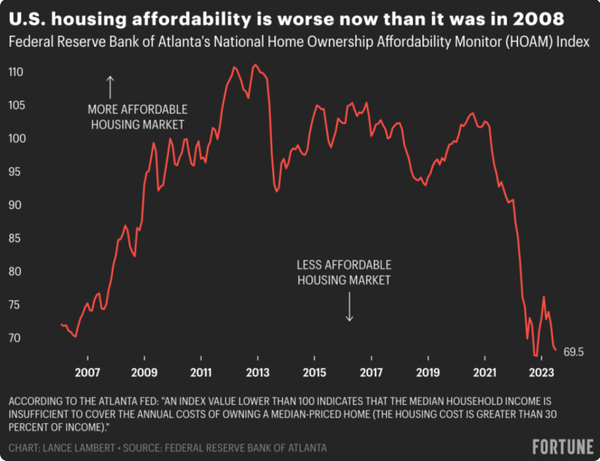

August Newsletter-What's causing the affordability issues

August newsletter. It’s almost back to school for the kids. Hopefully everyone has had a wonderful summer. I’ve been having fun helping some folks find quality homes. Last month I talked about how to back solve the affordability problem that is going on in the market, and picking the moment to move when the high interest rates eventually drop before that 5.5% point. This month I did a deep dive into why we’re in an affordability crisis, and how we got here. It gives us a good idea of what the obstacles we face for affordable housing, and how this impacts house pricing. It’s a kaleidoscope of problems. We’ll start back in 2008, aka the Great Recession, where bankers played loose with the mortgages, and the subsequent fall out from that. The government propped up the banks that were at the heart of the problem but failed to support the building professionals that worked in the industry that designed, created, and built it. It was a bleak time, we lost about half of the professionals & small-time builders. Most of these folks never came back to the industry, and to be honest why should they. Once bitten, twice shy. This dramatically reduced our capacity to build as a nation & a region. We’ve been slowly building back up businesses, but it’s not where it should be. At the local level the big issue from an affordability standpoint is how the building departments are funded. The building departments tend to be 100% funded by permit fees. When you add up all the fees for Washington County or the City of Portland for a new house it’s about $50,000-$70,000. Jurisdictions like to have the developers fund infrastructure building, for example curbs, sidewalks, and street improvements. This adds to the cost of the total project, and the total sale price of a project. This July, the City of Portland BDS raised it permit fees by 5-10%, and Washington County raised it permit fees by 50%. If we as a community want to bring down the cost of building, these programs need to be entirely tax funded, and the jurisdictions needs to be building the public infrastructure. The cost of new construction directly plays into the affordability of housing, when it costs more to build something new, it makes the existing homes on the market worth more. If we can take these costs out of the equation, we can reduce how much developers need to sell a house to make a profit which will in turn bring the markets affordability down. On a federal level President Trump, put into place a bunch of tariffs in 2018 with the good majority of these effecting the building industry either through raw materials, parts, machinery, and other supplies. The tariffs are as follows, Wood 20%, Steel 25%, Aluminum 10%, parts made of steel 25%, machinery 25%, and the list goes on. The impact of these tariffs directly raises the cost of new construction, hence increasing the value of all the existing buildings, and pushing affordability up. Below is a graph of the increase of the value of homes since 2016. Some of this increase was affected by supply chain shortages from the Covid pandemic but adding a 20-25% markup to the materials of a house doesn’t help. President Biden has largely left these tariffs in place, except for reducing the tariff on wood by 10%. It’s generally regarded that these tariffs have hurt our economy, and I would argue that it’s had a direct impact on the affordability of homes. Is China or the other foreign entities paying the tariff, the answer is no, we as the consumer pay for it. The 20-25% markup gets paid to the federal government, so as much as anyone in the federal government talks about solving the housing affordability issue, the biggest thing they could do would be to remove these tariffs. There’s some argument that the Urban growth boundaries has contributed to supply problems. I would say yes, and no. For the large tract builders, it’s limited how much they can build. After spending 23 years in the building industry, I’m not impressed with the quality of homes from DR Hortons, Lennar or Toll Brothers to name a few. Smaller builders the urban growth boundary has less of an impact on, as these folks are building on individual lots that are already established within the City. You could argue that the smaller builders are better for our local economy as well. As more of the money is being kept in the community by the smaller builders than those national builders that have headquarters and management located elsewhere. Another impact that’s driven up prices the impact of large investor groups buying up the single-family home and turning them into rentals to provide a return to the investors. This shrinks the available housing stock and pushes up prices. The whole law of supply and demand and how it drives the price of goods. There are many benefits to owning rental property for acquiring wealth, I think smaller investors are great, and healthy for the industry. Typically, most smaller investors are local and the money stays in the community. Generally, these large investment groups are in other parts of the country, and the money is leaving the community to be spent elsewhere. I’ll briefly touch on the Building Code, and I’ll preface this section by saying I think the building code is necessary from a life safety perspective and is good for the health and safety of our communities. However, the code continues to get more complex over the last 20 years. I agree with increasing insulation in buildings & R values in windows. However, I think there needs to be work done to simplify the code to reduce the complexity of it from the professional design standpoint, and from the code enforcement requirements. The American Society of Civil Engineers estimates that the number of engineers nationwide is decreasing each year. Moody’s estimates that the industry will need to create an additional 883,600 jobs by 2030. There’s a bit of a disconnect in the numbers if we continue this trajectory, we’re going to have a labor shortage that’s going to weigh on affordability. The last big contributor going on with affordability is the high interest rates, last week we hit a 22 year high for mortgage rates. This is well reported in the media, so I don’t feel like I need go further into it, but it’s huge problem for the building industry. Maybe not for the big builders who bake this into the home price, but for everybody else in the industry it’s a problem. My concern with this continued pressure is that the Fed is going to put a lot of the smaller businesses out of business, like what happened in 2008. I understand the commercial side of the business is hurting worse than the residential side of the industry. My concern is if the Fed bludgeons the industry the industry with high rates, we lose even more professionals to something else in a downturn, and instead of being the little engine that could, were the little engine that can’t. Governor Kotek’s team has pitched opening wetlands for building areas and getting rid of Portland’s tree removal fee ordinance. I don’t think either of these are decent solutions, and are rather short sighted. Building on wetlands opens up to a litany of long-term problems in a building and reduces areas of ever shrinking habit for some of four legged and winged friends. The tree removal program isn’t perfect, but it does encourage replanting of trees for the tree that are cut. This helps the beauty of our city as well as reduce heat in the summer. If I missed some other contributing factors, please let me know what you think I missed. The more I’m informed the better I’ll be able to help you all. Without the Fed crushing the building industry I don’t see a way for the affordability to get better without improving one or all these other factors. Hopefully, we’ll see some changes at the Local, State, and Federal levels that can bring the affordability problem into check. I’ll keep you up to date what shifts I’m seeing as the market adjusts. The interest rates dropping will have the biggest & fastest impact on affordability. All these other issues will help affordability if they can be resolved, but there will be a lag in time on how it affects the pricing of the market. Till next month! Have a great Labor Day weekend and stay safe. I’ll be hosting a US Open viewing party September 10th to watch the Men’s Final at the Eleete office downstairs lounge. There’s like eight or so screens, anyone is welcome to come. I’ll do some sort of food and drink.

Read More

July Newsletter

The real estate market is not like most markets where we show up and we can generally get what we want without competition from other consumers. To get a house that you want to purchase you’re competing with other buyers (especially in this market), and the best offer for the seller gets taken. Competition is the key word here. Most of you that know me well, know that I have a competitive side that I exercise with tennis, golf, chess, a game of cards or racing down the ski slopes. Let me digress before I come back to the point I’m trying to make. The biggest factor that is affecting the housing market is affordability. It’s what keeping homeowners with a 4% or below mortgage rate staying put or it’s buyers who can’t afford to purchase the type of home they want with the high interest rates. Its why existing homes sales are at about 50% from where they were in 2019 when were more in a typical housing market. There’s no sugar coating that the market is a bit stagnant with the current conditions of low inventory, but enough buyers not effected by rates to keep the prices stable in the metro area. There’s a term in engineering that we use, it’s called back solving. It’s what it sounds like, solving an equation backwards with a different given variable(s) or a different starting point. So, let’s back solve the market so it works for you! Why? Now this is where I get back to my original point of competition. It feels like we’re close to the peak or reached the top of the Fed rate hikes. After these rapid rate hikes, you’ll see the Fed drops the rates rapidly (see graph below). The steeper the rate hikes, the steeper the drops. I mentioned a few newsletters back that 71% of prospective buyers are waiting for an interest rate of 5.5%. So, here's the competition aspect of the market, and whether you want to compete with that volume of a buyers in the market. My fear is that we have a repeat of the summer of 2020 to the summer of 2022 when this log jam breaks open. Where there was a huge surge in prices because of the competition, and most buyers had to go above asking, waive inspections and offer “as is” to get an offer accepted. Decades ago, I was an Eagle Scout, and the Scouts motto is “Be Prepared” which is a great motto for life. I didn’t get in this business to be a salesman, I moved over to Real Estate from structural engineering to use my background, knowledge, and skill set to help people. If you’re thinking that you’d like a move in the next year or so, let’s have a conversation and get you prepared to navigate the market with less competition when the market hits the conditions that favor you. I’m here to help, and you’re not wasting my time. If you’re a skier you know that you need to prepare your gear ahead of time, watch the weather, and go when it’s a powder day! The only people that benefit from a crazy housing market are sellers that are moving out of state or are going to sit out for a couple of years. Recent Home tip is about damage caused to foundations from a leaky spigot in the summer months. Check it out on my website. www.nathanaustinrealtor.com

Read More

What the Market is doing in April.

Our expectations regarding the market incentives created by low interest rates came into focus in the first 13 weeks of the year, with listings (supply) off sharply from the year prior. We ended the quarter with the gap between this year and last growing wider, a signal that appears to indicate continued low transaction velocity heading into 2Q. This lack of supply appears to have stabilized pricing, and along with seasonal adjustments that look familiar, both median price and percent paid to asking bottomed in January and improved in February and March. Properties below the median now sell, on average, for 100.3% of asking price. Days on market also declined month-over-month for the entirety of the first quarter, now down 18% from the high in January. On the all-important subject of interest rates, inflation continues its steady (but slow) decline, and the last several months give reason to believe we are largely past rate increases. Below we see the annualized rate of inflation, average 30-year mortgage rate, and the real world rate taken by subtracting the yield on the 30-year mortgage from inflation. For nineteen months real world rates remained negative, that is the return on a 30-year mortgage was less than the rate of annualized inflation. As inflation fell and rates rose, real world rates turned positive in December and continue to improve. This is a welcome indication that interest rates are stabilizing and will fall along with inflation as we progress through the year. Bottom line: - The influence of low interest rates on sellers continues to impact supply - Buyer demand remains strong – absorption is in the 95-100% range and DoM is falling - Properties now sell on average for 100% of asking price - Without additional shocks to the system (i.e. bank failures, etc.), interest rates appear to have stabilized and there is a solid basis for expecting them to fall in the coming months - Housing is not going to become more affordable in the near future, as prices are reacting quickly to lack of supply and abating rates Stable pricing and low velocity – we have an interesting year ahead.

Read More

Recent Posts